Stacks Market V2: Redefining Lending and Borrowing

3

minute read

May 12, 2026

Zest Protocol

Since launch, Zest Protocol has hit several milestones that firmly established it as the leading DeFi protocol on Stacks:

- Roughly 15% of all sBTC on Stacks is deposited on Zest (~680 sBTC)

- Both total deposits and borrowing activity peaked at $100M+ and ~$10M respectively

- More than $9M in stablecoin liquidity has been unlocked

- ~25% of Stacking DAO LSTs deposited

- A growing suite of yield strategies now built on top of Zest Protocol

With this base in place, Zest v2 is the logical next step.

The protocol has already shown strong usage and clear product–market fit. The priority now is removing the bottlenecks that limited capital efficiency in v1.

V2 does this by reworking how risk is defined and managed, giving the market more security, more accuracy, and far more flexibility than before.

Before looking at the changes, it’s worth revisiting where v1 created bottlenecks.

The Bottlenecks of Zest v1

Similarly to Aave v3, Zest v1 relied entirely on collateral-centric risk parameters.

In practice, this meant, each collateral type (sBTC, STX, stSTX, etc.) had one LTV, one liquidation threshold, one liquidation penalty, and those same values applied regardless of which debt asset was borrowed.

For instance, if sBTC had a 70% LTV, that 70% applied whether the user borrowed USDC, USDh, STX, stSTX, or anything else..

This became a bottleneck because different debt assets behave very differently:

- Borrowing USDC against sBTC is relatively low-risk.

- Borrowing USDh has slightly more liquidity and peg risks.

- Borrowing volatile assets like STX is considerably riskier; STX can moon where users with STX debt get liquidated fast.

Because Zest v1 treated all debt assets the same, we had to configure conservative parameters to be safe in every market scenario; even when most pairs didn’t need that level of caution.

These conservative parameters resulted in low borrow caps, volatile debt driving protocol-wide risk limits and capital efficiency constrained by worst-case scenarios.

Zest has already proven to be the best in the game at setting the right parameters, and the proof is clear: over the past 1.5 years, more than 1,500 liquidations have been executed with zero bad debt.

That track record is a clear reminder of why Zest is the backbone of Stacks DeFi.

Zest v2: Redefining Risk

Zest v2 rethinks this model entirely; taking some of the cutting edge innovations from lending on Ethereum and Solana to the largest Bitcoin L2.

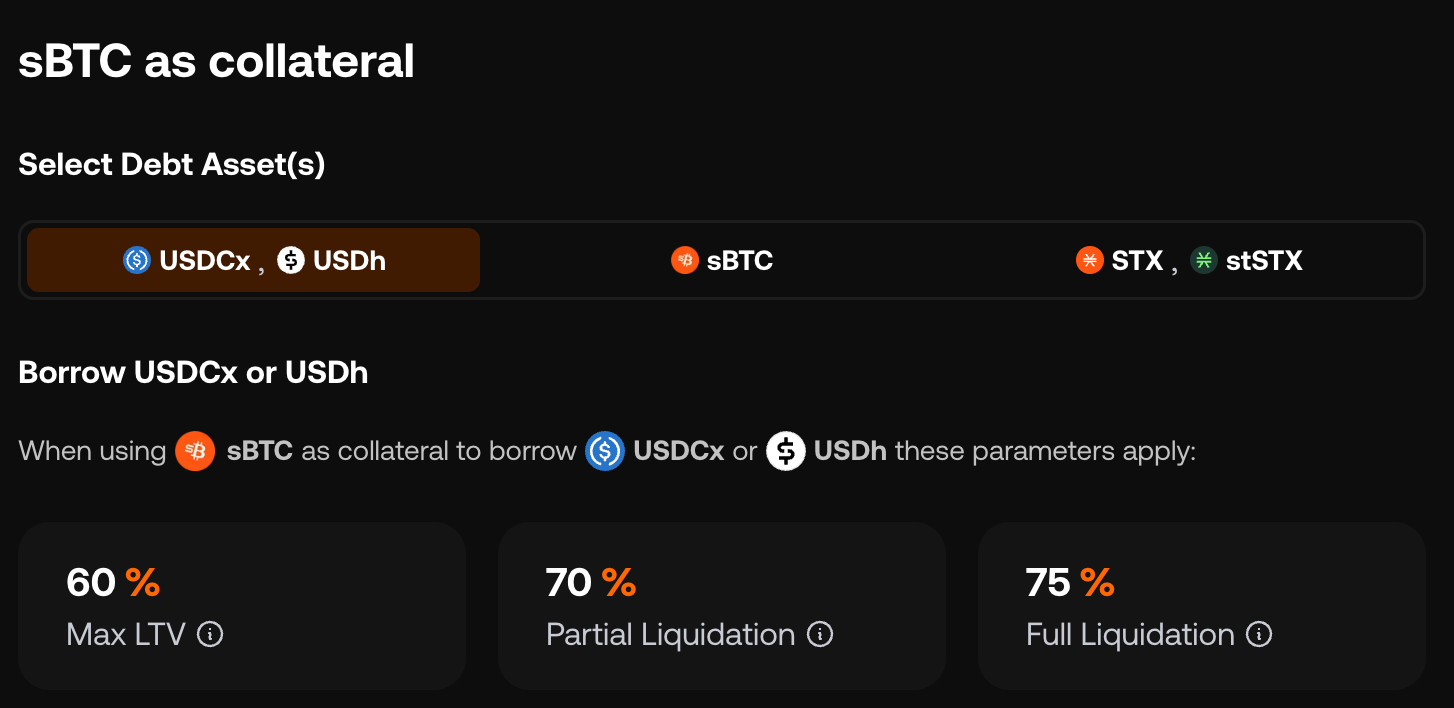

In v1, each collateral asset had a single set of risk parameters that applied to every loan against it. In v2, risk is defined per pair instead. This is where Risk Groups come in.

A Risk Group links a specific collateral asset to a specific debt asset. Each pair gets its own LTV, liquidation thresholds, penalties, and other settings, all tuned to how those two assets actually behave together.

Let’s illustrate this with an example. Under the v1 model, STX borrowing had to be constrained because the system permitted loans at a 70% LTV against sBTC, exposing the protocol to excessive liquidation risk.

Under v2, with Risk Groups in place, each pair can be set appropriately:

USDC borrowing is assigned a 70% LTV and an 85% liquidation threshold against sBTC, reflecting its lower volatility.

While STX can be limited to a 30% LTV and a 65% liquidation threshold against to account for sharper price movements in STX and the potential for more frequent liquidations.

In other words, each collateral to debt combination can finally be configured on its own terms, rather than forced into a single, protocol-wide template.

The benefits follow naturally:

- Far better capital efficiency

Stable to stable or tightly correlated assets can support higher LTVs without increasing protocol risk. - Safer handling of volatility

Volatile to volatile combinations get lower LTVs and earlier liquidation thresholds, allowing for an even safer system. - Higher borrow caps

Because risk is isolated per pair, less volatile assets can be borrowed much more aggressively without increasing risk. - Easier onboarding of new assets

USDh, stSTX, and future assets can be added with parameters tailored to their behaviour rather than constrained by others. - Parameters that match reality

Borrowing USDC against sBTC is nothing like borrowing STX against sBTC. Risk Groups finally allow the protocol to treat those cases differently; users get liquidated less frequently as a result. - Best in class security

V2 has undergone multiple audits, building on what was already the most reviewed Stacks protocol. The migration will follow established best practice, offering a one-click flow from v1 to v2 and aligning with the aeUSDC–USDCx migration to keep the process smooth.

In conclusion, v2 sets the foundation for a lending market that can scale with new assets, new strategies, and growing demand across the Stacks ecosystem. Learn more about Risk Groups and Parameters here.

Additional Upgrades in v2

With the Stacks Market v2, Zest also introduces two huge new upgrades:

1) Smoother Liquidations

In v1, once a position crossed the liquidation threshold, the entire position was liquidated at once.

v2 replaces this with a more predictable, controlled model built around a liquidation slope (partial → full) and an exponent curve, which delivers:

- Fewer sudden “cliff” liquidations

- A smoother, more predictable process

- A safer environment for liquidators

- Stronger systemic stability

- Relying on Pyth for reliable and precise pricing data

Every collateral–debt pair now has both a partial and a full liquidation threshold. This smooths the process and gives users time to add collateral or repay.

For example, with sBTC as collateral and USDC as the borrowed asset, partial liquidations begin at a 85% LTV, while full liquidation occurs at 95%.

The penalty is no longer fixed either; it now varies between a minimum and maximum range to provide additional protection. You can learn more about Liquidations in the Zest Docs.

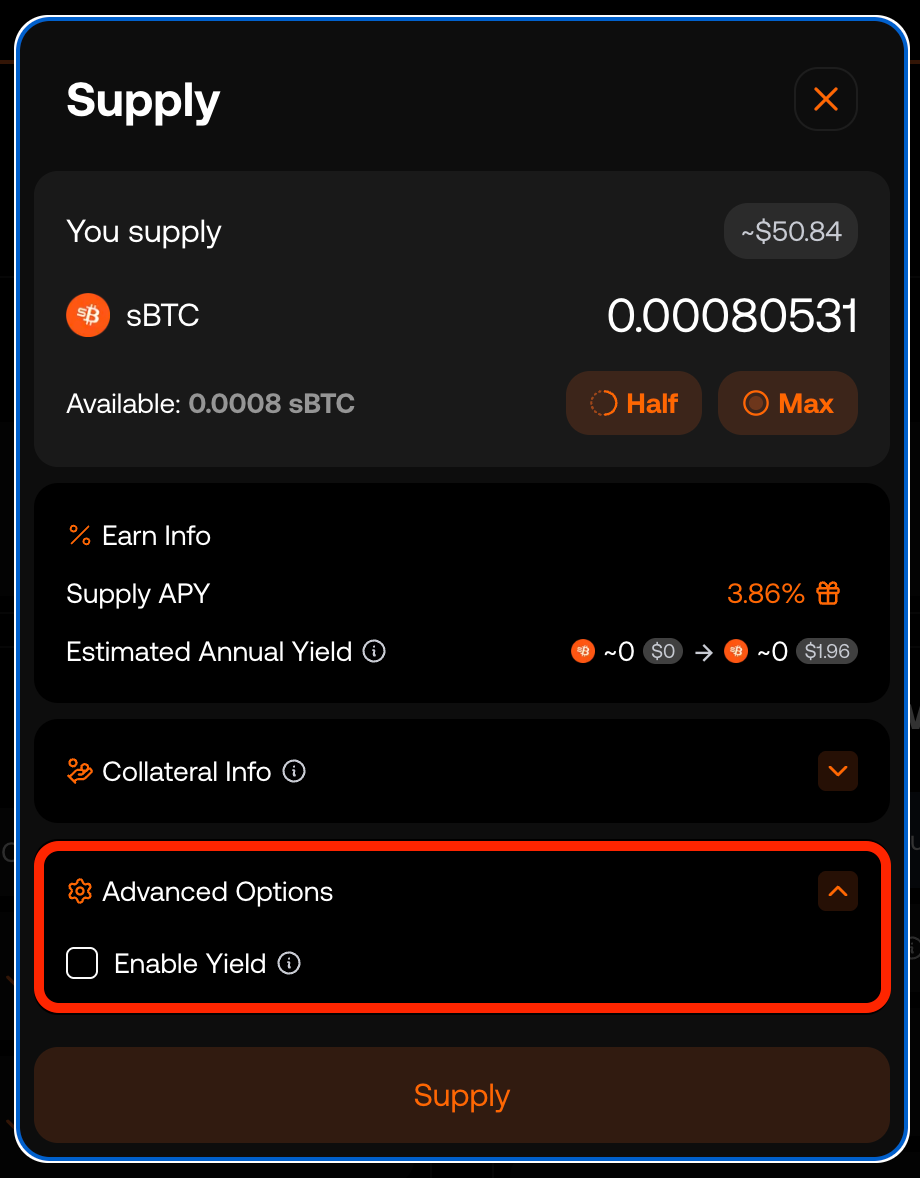

2) No rehypothecation

With this new feature users can opt for an added layer of security: their deposits can remain strictly segregated as their own collateral and never be lent (so no yield is earn on the deposit), giving them clearer risk boundaries and greater control.

How To Get Started

Getting started with v2 is straightforward.

When you open the Zest Protocol app, you’ll see a pop-up prompting you to migrate your existing position to the v2 market in a single transaction. If you prefer step-by-step guidance, a guide is available in the docs.

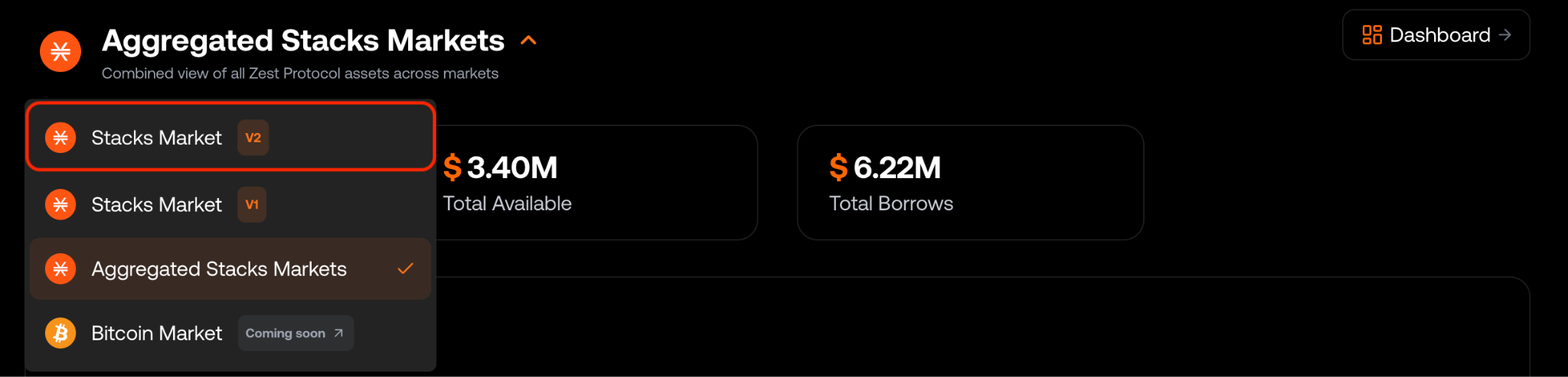

You can also migrate manually by closing any borrowing positions on v1, withdrawing your liquidity, and then depositing it into v2. Switching between v1 and v2 is simple: use the market selector in the top-left corner of the interface, as shown below.

Finally, you can always explore the documentation to learn more about v2 and the different risk groups.

About Zest

Earn yield and borrow assets on Zest protocol.

Follow us on Twitter for all of the latest updates and memes!

Join our community via Discord!

And as usual, stay zesty🍊